THE FED'S DUAL MANDATE:

12 U.S.C. § 225a.

The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.

HAVE THEY BEEN GOOD AT EFFECTIVELY PROMOTING MAXIMUM EMPLOYMENT? NO.

HOW ABOUT STABLE PRICES? NO AGAIN.

Could you stay in your job if you were as incompetent as these guys are? I don't think so.

These guys need to be replaced. Fired. And if they don't like it, take them off in handcuffs or chains. And bring back prisoner torture until they are tried and convicted for their thievery and economic mischief.

Because QE1 was such a rousing success, this week the Fed has let on that they are now considering a round of QE2. The hair of the dog that bit you to cure a hangover. Works every time. Fixes the hangover, does nothing for the underlying alcoholism.

Their twisted economic theory that says we should rob wealth from the poor, the elderly on fixed income, the savers to protect the bankers, Wall Street and the rich via the hidden stealth tax increase that is inflation. They are openly destroying the dollar to prop up asset prices.

But not the assets that the middle class owns, like their homes.

This is like a reversal of the Robin Hood economic theory of robbing from the rich to give to the poor. Bernanke believes the poor and the middle class should pay to protect the financial system. Just like his scum-bag acolytes like Charlie Munger and Warren Buffet.

The guys should all hang together. Literally.

Here is what the Fed has done to the value of the dollar in their 97 years at the helm. A 97% depreciation rate. At that rate, the dollar will not only be WORTH LESS (two words) in three more years, it may become WORTHLESS (one word).

The threat of QE2 was met with mixed reviews.

The best review I heard was that the Fed can print money, but they cannot figure out how to print jobs. In theory, if they were able to, they would have done so by now.

"When the Fed buys long-term government debt from the private market, it shifts interest rate risk from bondholders to taxpayers," Minneapolis Fed President Narayana Kocherlakota warned last week.

Philly Fed President, Charles Plosser agrees: "Asset purchases in our current economic environment can do little if anything to speed up the return to full employment," Plosser said in a speech last week. "Because I see little gain at this point, and some costs, I would prefer not to engage in further asset purchases at this time."

"We are following policies that unless changed will eventually lead to lots of inflation down the road," said Warren Buffett at Fortune’s Most Powerful Women Summit Tuesday. "We have started down a path you don’t want to go down."

Chicago Fed’s Charlie Evans disagrees (and he’s a voting member next year!) and said yesterday that he favors "much more [monetary] accommodation than we’ve put in place." MUCH MORE than $2Tn - take that Japan and your puny $500Bn pledge!

All the things we own, going down in value. Effectively being destroyed by these thugs.

All the things we pay for, food, fuel are going to go up in price. Commodities, the inputs for most of the things the middle class consumer needs, have skyrocketed on just the mention of another round of this failed Quantitative Easing policy.

Oil is heading back towards the $90-$100 a barrel level. Say hello to $5 / gallon gasoline.

Agricultural commodity prices have skyrocketed.

Don't worry we don't count oil and food costs in calculating CPI.

Our government is morally bankrupt as well as financially bankrupt.

The congress can no longer dip into the peoples wallet for Stimulus2 because:

a) we have elections and

b) the government is broke.

But the Federal Reserve is not elected, yet they have the future of the American economy in their hands.

Never mind what happened the last time Bernanke did this. He cranked up commodities through the same crap with the dollar and triggered the worst of the slowdown economically in terms of its impact on ordinary people, because energy and commodity prices ramped.

We keep making the same mistakes by repeating the same failed policies. Rinse, lather, repeat. The definition of insanity.

Piling more debt upon an already unsustainable amount of debt no longer works. The whole law of diminishing returns. Households know this, you can't get out of debt by paying your bills with a credit card.

Consumers are deleveraging, they are tired of being in debt. They are starting to understand those old-school phrases like "Neither a borrower nor a lender be" and "the borrower is a slave to the lender". Good for them.

They have daily experience with the inherent evils of "usury interest" whenever they open their credit card statements and are just now beginning to see why the system of "fractional reserve banking" is no longer magic. You can't create money out of thin air endlessly. The system collapses upon itself like a house of cards. Like a Ponzi scheme. They all unravel eventually once you run out of suckers and fools. And I think finally, American are tired of being played for fools.

Kevin Duffy of Bearing Asset Management described the process very well back in a 2007 article titled, 'IT'S A MAD, MAD, MAD, MAD WORLD' :

Yes, indeed it is.

Fractional reserve madness

The lure of easy money begins with the government printing press. First, the central banker buys an asset typically a government debt instrument writes a check on itself and deposits it into the banking system. Since the bank never "redeems" the check, this is equivalent to creating money out of thin air. The banker, happy to receive fresh "reserves", loans out all but a sliver. This new money ends up back with the banks, is counted again as reserves, mostly lent out, and so on and so on.

Through this process of fractional reserve banking, credit is expanded at a multiple of the initial central bank deposit. Through such a system, the creation of money and credit (the promise to pay money) looks like an upside-down pyramid - essentially a pyramid scheme on top of a counterfeiting operation.

As James Grant has counseled, the inflation process gives a finite pool of capital the illusion of an endless sea of liquidity, in effect "turning all the traffic lights green."

Such a scheme is a concoction of government privilege (or mercantilism), not laissez faire. The so-called "capitalists" are no longer efficient allocators of capital to its most productive uses, but beneficiaries of and cheerleaders for a monetary fraud in which capital is debased, taken for granted, abused. As long as they remain chummy with their friendly liquidity provider of last resort, they can act recklessly without fear of igniting an economic forest fire or if they do, without fear of having to bear the costs. And as long as the value of their collateral is constantly inflated, they never feel the need to worry about default.

Liberated from the gold standard straightjacket, the system has few restraints. For starters, the counterfeiter has an incentive not to draw attention to his racket. But the effectiveness of his ongoing propaganda campaign has weakened this deterrent. The real inflationary action, however, is in credit expansion. For example, in the last 6 years, the Federal Reserve has grown its balance sheet less than $300 billion while the nation's money supply has expanded by $4.3 trillion, or 14 times as much. In other words, the central banker can bait the hook, but lenders and borrowers still have to take the bait.

This new money is never evenly distributed, but instead gets funneled into whatever narrow area happens to capture the public's fascination. As prices and valuations soar, greater doses of credit are required to keep the game going. Either more marginal borrowers are drawn in at ever more precarious levels or greater leverage must be applied to existing borrowers. This is what ultimately doomed the housing bubble. In the end, nearly anyone who could fog a mirror was getting an invitation to join the party.

The trouble with pyramid schemes is that they're not designed to go in reverse. Eventually, the number of willing dupes is exhausted. The same people who panicked late to get into the game are just as likely to panic when the music stops. The longer the music plays, the more leveraged and unstable the inverted credit pyramid becomes. As the late economist Hyman Minsky observed, "stability is unstable."

I love these two analogies of the fallacy of QE2 from Richard Koo, the Chief Economist of Nomura Research Institute:

In describing the negligence of such monetary policy Richard Koo uses the analogy of a doctor who simply tells his patient to take more of the same medicine he originally prescribed:

“At the risk of belabouring the obvious, imagine a patient in the hospital who takes a drug prescribed by her doctor, but does not react as the doctor expected and, more importantly, does not get better. When she reports back to the doctor, he tells her to double the dosage. But this does not help either. So he orders her to take four times, eight times, and finally a hundred times the original dosage. All to no avail. Under these circumstances, any normal human being would come to the conclusion that the doctor’s original diagnosis was wrong, and that the patient suffered from a different disease. But today’s macroeconomics assumes that private sector firms are maximizing profits at all times, meaning that given a low enough interest rate, they should be willing to borrow money to invest.. In reality, however, borrowers – not lenders, as argued by academic economists – were the primary bottleneck in Japan’s Great Recession.”

Dr. Bernanke has misdiagnosed this illness one too many times. At what point does someone tell him to put the scalpel down and step away from the table before he does even greater harm?

Koo describes the failure of QE1 as a tool to promote economic recovery in the following. Mr. Koo is keenly aware of the the experience of a Quantatative Easing strategy as it has been applied in Japan for the last decade or more. It has been roundly noted as a dismal failure.

Koo goes a step further in describing the failure of QE to promote private sector recovery.

“The central bank’s implementation of QE at a time of zero interest rates was similar to a shopkeeper who, unable to sell more than 100 apples a day at $100 each, tries stocking the shelves with 1,000 apples, and when that has no effect, adds another 1,000. As long as the price remains the same, there is no reason consumer behavior should change–sales will remain stuck at about 100 even if the shopkeeper puts 3,000 apples on display. This is essentially the story of QE, which not only failed to bring about economic recovery, but also failed to stop asset prices from falling well into 2003.”

This mea culpa came from Ambrose Evans-Pritchard of the Telegraph (UK):

http://blogs.telegraph.co.uk/finance/ambroseevans-pritchard/100007777/shut-down-the-fed-part-ii/

I apologise to readers around the world for having defended the emergency stimulus policies of the US Federal Reserve, and for arguing like an imbecile naif that the Fed would not succumb to drug addiction, political abuse, and mad intoxicated debauchery, once it began taking its first shots of quantitative easing.

My pathetic assumption was that Ben Bernanke would deploy further QE only to stave off DEFLATION, not to create INFLATION. If the Federal Open Market Committee cannot see the difference, God help America.

We now learn from last week’s minutes that the Fed is willing “to provide additional accommodation if needed to … return inflation, over time, to levels consistent with its mandate.”

Ben Bernanke has not only refused to abandon his idee fixe of an “inflation target”, a key cause of the global central banking catastrophe of the last twenty years (because it can and did allow asset booms to run amok, and let credit levels reach dangerous extremes).

Worse still, he seems determined to print trillions of emergency stimulus without commensurate emergency justification to test his Princeton theories, which by the way are as old as the hills. Keynes ridiculed the “tyranny of the general price level” in the early 1930s, and quite rightly so. Bernanke is reviving a doctrine that was already shown to be bunk eighty years ago.

and this

So all those hillsmen in Idaho, with their Colt 45s and boxes of krugerrands, who sent furious emails to the Telegraph accusing me of defending a hyperinflating establishment cabal were right all along. The Fed is indeed out of control.

The sophisticates at banking conferences in London, Frankfurt, and New York who aplogized for this primitive monetary creationsim – as I did – are the ones who lost the plot.

My apologies. Mercy, for I have sinned against sound money, and therefore against sound politics.

Fed is trying to conjure away the hangover from the last binge (which Greenspan/Bernanke caused, let us not forget), as if to vindicate its prior claim that you can always clean up painlessly after asset bubbles.

Are the Chinese right? Are the Americans and the British now so decadent that they will refuse to take their punishment, opting to default on their debts by stealth?

It does seem as if the Euro is being rewarded for taking their governments and Central Bank taking the path of fiscal austerity and sound monetary policy. At least for now. I don't see how intentionally torching your currency can be the answer to what ails the American economy. And it is not worth the costs it will impose on the poor and those who saved and invested prudently. Profligate spenders and gamblers are being protected and rewarded.

So we have these Fed idiots disguised as experts, protecting their own special interest under the guise of protecting the middle class. I call BS on that one. They don't give a rats fat ass about the middle class. None of them.

And as the Obama administration continues to hemorrhage economic advisers, I can only advise the President to consider taking the term "heads are going to roll" more literally Romer, Orzag, Emmanuel (not an eco advisor) and Lawrence Summers have all beat a hasty retreat.

To be followed soon by the incompetent, criminal Secretary of Treasury Geithner. Hopefully, no later than the soon after the elections. He doesn't have the confidence of this country's business community, the international community, heck he doesn't get respect around Chinese school children. That should have told you all you needed to know about old Turbo Timmy. And he calls the Chinese currency manipulators when the Federal Reserve is doing it's own brand of manipulation.

This from the blog The Economic Collapse:

http://theeconomiccollapseblog.com/archives/federal-reserve-officials-americans-are-saving-too-much-money-so-we-need-to-purposely-generate-more-inflation-to-get-them-spending-again

Does increasing inflation as a way to stimulate the economy sound like a good idea to any of you?

These are supposed to be some of the brightest economic minds that our nation has produced.

Unfortunately, it is becoming increasingly apparent that the folks running the Federal Reserve do not have a clue about sound economic policy.

Anyone who lived through the "stagflation" days of the 1970s should know that inflation does not spur economic growth.

But now some of the most prominent Fed officials are publicly proposing that we should purposely generate more inflation so that "real interest rates" (interest rates with inflation factored in) will go down.

For example, during a recent interview the president of the Federal Reserve Bank of Chicago, Charles Evans, made the following statement....

"It seems to me if we could somehow get lower real interest rates so that the amount of excess savings that is taking place relative to investment needs is lowered, that would be one channel for stimulating the economy."

If you truly grasp what Evans is proposing here, your jaw should be dropping.

He is basically coming right out and saying, "Hey, let's go out and crank up the inflation rate so that American consumers will start recklessly spending their money again."

So are Americans really saving too much money?

Of course not.

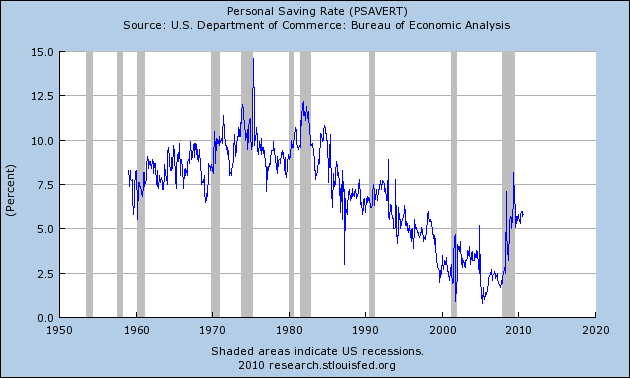

Just take a look at the chart below.

Americans are actually still saving far, far less than they used to. As you can see from the chart, in the 1960s and 1970s Americans would usually save somewhere between 8 to 12 percent of their incomes.

Today, we are still well below that level. But we have made some progress from the reckless days of five to ten years ago when Americans were living far, far, far beyond their means and basically saving next to nothing....

So now some top Fed officials want to undo all that. They apparently want Americans to grab their credit cards and to run out to the stores and spend wildly like they did a few years ago.

But spending recklessly is not going to repair our economy. In order to have a healthy, balanced economy you need to have a healthy personal saving rate. Encouraging Americans to spend every last nickel they have may boost economic figures in the short-term, but it will make our long-term problems even worse.

These guys need to get it together rather quickly before there's Revolution in this country.

Hopefully, it's a peaceful one.

No comments:

Post a Comment